.png)

Individual Tax Series: Basic Personal Amount and Spousal Tax Credit: Understanding and Maximizing Your Tax Benefits

- Rylan Kaliel

- Jun 25, 2025

- 7 min read

Updated: Jul 7, 2025

In Canada, tax credits play an essential role in reducing your overall tax liability, helping keep more money in your pocket. Two fundamental credits available to Canadian taxpayers are the Basic Personal Amount and the Spousal Tax Credit. Understanding these credits, who qualifies, and how to claim them can significantly impact your financial outcomes at tax time. This blog will clearly explain these important credits and how you can maximize their benefits.

What is a Tax Credit?

Tax credits are a direct reduction to your taxes payable. As was discussed in our Basics of Individual Taxation blog post, there are multiple level of deductions, with tax credits coming right after the initial calculation of taxes payable. When we calculate taxable income, we multiply these by the effective tax rates to determine our taxes payable, before credits, then subtract our tax credits to determine our actual taxes payable.

As we can see above, we had originally calculated taxes payable of $26,754, however, our tax credits reduce this to $21,916, a decrease of close to $5,000 in taxes payable.

How are Tax Credits Calculated?

Most tax credits are calculated at the lowest tax rate applicable to an individual. Federally, this is 15% (however, changes to this rate may reduce this to 14% effective July 1, 2025). This means that for each $100 of tax credits you save $15 of tax. There can be exceptions to this, particularly with donation and dividend tax credits (discussed in a later blog post), however, the general rule is that the lowest tax rate would be applicable.

Prior to this calculation, all tax credits that have this lowest tax rate are totaled and then this total is multiplied against this tax rate. Let’s look at this in action.

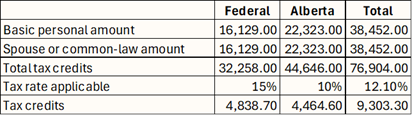

As we can see, we group the basic personal amount and spouse or common-law amount to get our total tax credits. This total is applied against the tax rate to determine the federal tax credits.

You’ll note, we indicate that this is the federal tax credits. We note this as there are both federal and provincial tax credits, which can vary in amounts. Let’s look at a combined federal and provincial tax credit analysis.

You’ll note in the above that Alberta, used as an example, has a higher tax credit, but also has a lower tax rate applicable. The lower tax rate is due to the lowest tax rate in Alberta being lower than the federal tax rate, a common occurrence in Canada. This results in the average tax rate applied to all tax credits being closer to 12%.

Non-Refundable Tax Credits

This term will be used throughout this blog post and into future blog posts, so it is important to know. A non-refundable tax credit means that if you can’t use the full amount, you lose it. Essentially, if you calculate your taxes payable, before tax credits, and it is less then the tax credits available, your taxes payable will be $0, not a negative amount.

In the above example, we see that we have taxes payable, before credits of $4,000, however, our tax credits exceed our taxes payable. This results in our taxes payable, after credits, being $0, rather than a refund of $839, by virtue of this non-refundable tax credit system.

What is the Basic Personal Amount (BPA)?

The Basic Personal Amount (BPA) is a non-refundable tax credit available to every Canadian taxpayer. It provides a tax-free threshold, ensuring individuals do not pay taxes on income needed for basic living expenses. The BPA reduces the amount of taxes you owe by directly lowering your taxes payable, before tax credits.

The CRA adjusts the BPA annually for inflation. For the 2025 tax year, the BPA is approximately $16,129 and provincially, using Alberta as an example, $22,323 (the exact amount changes slightly each year). This amount effectively represents the income threshold you can earn before paying any federal income taxes.

Let’s look at an example of this, let’s assume an individual made $15,000 of taxable income in the year.

As we can see in the above calculation, for both federal and provincial (using Alberta as an example) purposes, we have taxes payable, before tax credits that is less than the tax credits, resulting in taxes payable, after-tax credits of $0 (see Non-Refundable Tax Credits above for more details on why this is $0).

Given this, we can essentially rely on the BPA being the threshold that if your income is less than this amounts you do not have to pay taxes (however, see CPP and EI Considerations for other tax considerations).

Spousal or Common-Law Partner Tax Credit

The spousal or common-law partner tax credit (the “Spousal Tax Credit”) is available to taxpayers who financially support their spouse or common-law partner. If your spouse or partner has a significantly lower income or no income at all, you can claim this credit, reducing your overall taxes payable.

To qualify, your spouse or common-law partner must:

Have a lower net income than you.

Be living with you, or if separated due to medical or other necessary circumstances, still supported financially by you.

The Spousal Tax Credit is calculated based on the difference between your spouse’s net income and the basic personal amount. The calculation is:

Spousal Tax Credit = (Basic Personal Amount – Spouse’s net income)If your spouse earns $5,000 and the BPA for 2025 is $16,129, we expect the following calculations for the federal tax credit:

As we can see, we start with the basic personal amount and then reduce it for the spouse’s income. This leaves us with a tax credit of $11,129 which we can then apply the tax rates to and reduce our taxes payable.

Eligible Dependent Tax Credit

The eligible dependent tax credit is only available if you were unmarried and did not live in a common-law partnership or you were married or live in a common-law partnership, but you did not live with, support, and were not supported by your spouse. Essentially, you cannot be potentially eligible to claim the Spousal Tax Credit to get this credit.

The eligible dependent tax credit is only available if the dependent is:

Resident in Canada;

Your parent, grandparent, child, grandchild, brother or sister by blood, marriage, common-law partnership or adoption; and

Except in the case of your parent or grandparent, either under 18 years of age or dependent on you due to mental or physical infirmity.

The calculation of the eligible dependent tax credit is the exact same as the Spousal Tax Credit. Please see Spousal or Common-law Partner Tax Credit for details of this calculation.

Claiming the BPA and Spousal Tax Credit

These credits are claimed on your personal tax return, T1 Income Tax and Benefit Return:

The BPA is automatically applied to all individual tax returns.

The Spousal Tax Credit must be claimed explicitly, usually entered on Schedule 5 Amounts for Spouse or Common-Law Partner and Dependents of your T1.

Ensure accurate reporting by clearly documenting your spouse's income and supporting documents in case of a CRA review.

CPP and EI Considerations

Please note that we have indicated that there is a threshold in which you will not have to pay tax, such as having income below the BPA. While this is true for income tax, we must still consider the Canada Pension Plan (CPP) and Employment Insurance (EI) systems, which are discussed in our Understanding CPP and EI blog post.

CPP and EI are calculated using different rules then income tax, so the threshold for no taxes being payable are lower and they may not allow for similar deductions you’d get for income tax. As such, we should be careful to ensure that under all three systems there is no tax to guarantee this result.

Consider an extended example of an individual of $15,000 of income.

In the above, we have no income tax, which is expected and was demonstrated above. However, you’ll note that we have exceeded the basic exemption for CPP and EI, resulting in some tax owing for both. There are no tax credits under CPP and EI and as such, this tax remains outstanding. Therefore, we can still have taxes payable even if we are below the BPA.

Strategic Considerations for Maximizing These Credits

To maximize benefits from these credits:

Clearly identify and document the exact income of both spouses.

Strategically plan income splitting opportunities, if available, to ensure the lower-income spouse’s earnings remain within optimal levels for claiming the credit.

Common Mistakes and How to Avoid Them

Common pitfalls related to BPA and spousal credits include:

Missing the opportunity to claim the spousal credit when eligible.

Incorrectly reporting your spouse’s income.

Misunderstanding eligibility requirements (such as marital status definitions).

To avoid these issues:

Carefully verify your spouse’s income annually.

Ensure correct and timely completion of tax returns, particularly Schedule 1.

Consult a tax professional if you're uncertain about eligibility.

Impact on Other Benefits and Credits

Properly claiming the BPA and spousal tax credit can also influence eligibility for other benefits and income-tested credits, such as GST/HST credit, Canada Child Benefit, and provincial programs. Accurate reporting ensures optimal benefits.

Summary

Understanding and effectively claiming the Basic Personal Amount and spousal tax credit can significantly reduce your tax bill and enhance your family's financial stability. Staying informed about eligibility criteria, keeping detailed records, and accurately completing your tax return ensures you maximize your available tax savings.

Stay tuned for our next blog, where we'll explore the Canada Workers Benefit and how to optimize your eligibility.

KLV Accounting, a Calgary-based accounting firm, is here to help. Contact us today to enhance your financial strategy, minimize your taxes, and drive business success! For a free consultation, call us at 403-679-3772 or email us at info@klvaccounting.ca.

Comments